|

|

Provided to you Exclusively by Jim Belote

|

For the week of Mar 24, 2014 | Vol. 12, Issue 12

|

|

|

|

|

582 Lynnhaven Parkway, Suite 300

Virginia Beach, VA 23452

|

|

In This Issue In This Issue

|

|

|

|

Last Week in Review: The harsh winter weather throughout much of the country had a big impact on the housing market. Plus, the Fed met.

Forecast for the Week: Housing reports will be front and center, along with key news on inflation, economic growth, and consumer attitudes.

View: Sharing local statistics with clients and referral partners is easy with this resource.

|

|

Last Week in Review

|

|

|

|

Time for a change. With spring officially here, the change of season will hopefully lead to a change of direction for the housing market, as the harsh winter weather contributed to several disappointing reports.

February Existing Home Sales fell by 0.4 percent from January to 4.60 million units on an annualized basis. While this number was in line with estimates, it was 7.1 percent below the 4.95 million units registered in February 2013. The National Association of Realtors cited the unusually harsh winter weather, tightening of credit, and higher home prices as the cause behind the stagnant sales data. February Existing Home Sales fell by 0.4 percent from January to 4.60 million units on an annualized basis. While this number was in line with estimates, it was 7.1 percent below the 4.95 million units registered in February 2013. The National Association of Realtors cited the unusually harsh winter weather, tightening of credit, and higher home prices as the cause behind the stagnant sales data.

The harsh weather was also blamed for the weak Housing Starts reading for February, which came in at 907,000, making this the third straight monthly decline. In addition, the National Association of Home Builders Housing Market Index came in at 47 for March. Readings below 50 indicate that more builders view conditions as poor, rather than good. On a positive note, Building Permits, which are a sign of future construction, surged by 7.5 percent to 1.018 million. It will be important to see if readings improve once the weather becomes milder around the nation.

In other news to note, weekly Initial Jobless Claims rose by 5,000 in the latest week to 320,000. Claims continue to hover near lows seen in November, as the labor markets work through the post-recession malaise. The 4-week moving average, which irons out seasonal abnormalities, came in at 327,000, the lowest level since the end of November.

What does this mean for home loan rates? Despite some weaker than expected economic reports, the Fed announced more tapering to its Bond buying program. Beginning in April, the Fed will purchase $30 billion in Treasuries and $25 billion in Mortgage Bonds (the type of Bonds on which home loan rates are based) to help stimulate the economy and housing market. This is down from the original $85 billion per month that the Fed had been purchasing. I will be watching closely to see how this decision impacts the markets and home loan rates as we head further into spring.

The bottom line is that now remains a great time to consider a home purchase or refinance, as home loan rates remain attractive compared to historical levels. Let me know if I can answer any questions at all for you or your clients.

|

|

Forecast for the Week

|

|

|

|

This week's economic calendar is packed with important data on housing, inflation, and economic growth.

- Housing data is plentiful this week with the S&P Case-Shiller Home Price Index and New Home Sales being reported on Tuesday. Pending Home Sales follows on Thursday.

- We'll get a read on consumer attitudes towards the U.S. economy with Consumer Confidence on Tuesday and the Consumer Sentiment Index on Friday.

- Wednesday brings February's Durable Goods Orders, which are orders for items that last for an extended period of time.

- Weekly Initial Jobless Claims will be released as usual on Thursday. Also look for the final reading of Gross Domestic Product for the fourth quarter of 2013.

- Ending the week, the inflation-reading Personal Consumption Expenditures data along with Personal Income and Personal Spending will be delivered on Friday.

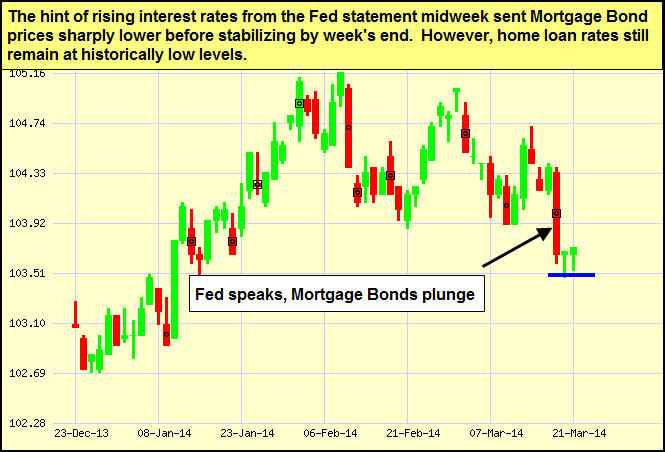

Remember: Weak economic news normally causes money to flow out of Stocks and into Bonds, helping Bonds and home loan rates improve, while strong economic news normally has the opposite result. The chart below shows Mortgage Backed Securities (MBS), which are the type of Bond on which home loan rates are based.

When you see these Bond prices moving higher, it means home loan rates are improving – and when they are moving lower, home loan rates are getting worse.

To go one step further – a red "candle" means that MBS worsened during the day, while a green "candle" means MBS improved during the day. Depending on how dramatic the changes were on any given day, this can cause rate changes throughout the day, as well as on the rate sheets we start with each morning.

As you can see in the chart below, Mortgage Bonds worsened after the Fed meeting but were able to stabilize. Home loan rates remain near historic best levels and I will continue to monitor them closely.

Chart: Fannie Mae 4.0% Mortgage Bond (Friday Mar 21, 2014)

|

|

The Mortgage Market Guide View...

|

|

|

|

|

Health Website Makes Sharing Local Data Easy

Gone are the days of extensive research, compiling information, and sharing numerous website links in order to provide local stats and health data with relocating clients and prospects.

Now, finding that information is quick and convenient with County Health Rankings. Through the collaboration of the Robert Wood Johnson Foundation and the University of Wisconsin Population Health Institute, the website brings together 50 diverse reports resulting in a health ranking for each county in the U.S.

How Does Your Community Rank?

1. Visit www.countyhealthrankings.org.

2. Select your state from the map.

3. Once the state map appears, select your county.

Within a few clicks, you can see your county's overall ranking, as well as other important local statistics such as:

- Population

- Unemployment

- Education

- Smoking and drinking

- Access to recreational facilities

- Air pollution

- Poverty

- Motor vehicle death rates

- Diabetes

- And much more!

Check your local stats and feel free to pass this resource along to your team, clients, and colleagues.

Economic Calendar for the Week of March 24 - March 28

Date

|

ET

|

Economic Report

|

For

|

Estimate

|

Actual

|

Prior

|

Impact

|

Tue. March 25

|

09:00

|

S&P/Case-Shiller Home Price Index

|

Jan

|

NA

|

|

13.4%

|

Moderate

|

Tue. March 25

|

10:00

|

Consumer Confidence

|

Mar

|

NA

|

|

78.1

|

Moderate

|

Tue. March 25

|

10:30

|

New Home Sales

|

Feb

|

NA

|

|

468K

|

Moderate

|

Wed. March 26

|

08:30

|

Durable Goods Orders

|

Feb

|

NA

|

|

-1.0%

|

Moderate

|

Thu. March 27

|

08:30

|

GDP Chain Deflator

|

Q4

|

NA

|

|

1.6%

|

Moderate

|

Thu. March 27

|

08:30

|

Gross Domestic Product (GDP)

|

Q4

|

NA

|

|

2.4%

|

Moderate

|

Thu. March 27

|

08:30

|

Jobless Claims (Initial)

|

3/22

|

NA

|

|

NA

|

Moderate

|

Thu. March 27

|

10:00

|

Pending Home Sales

|

Feb

|

NA

|

|

0.1%

|

Moderate

|

Fri. March 28

|

08:30

|

Personal Income

|

Feb

|

NA

|

|

0.3%

|

Moderate

|

Fri. March 28

|

08:30

|

Personal Spending

|

Feb

|

NA

|

|

0.4%

|

Moderate

|

Fri. March 28

|

08:30

|

Personal Consumption Expenditures and Core PCE

|

Feb

|

NA

|

|

0.1%

|

HIGH

|

Fri. March 28

|

08:30

|

Personal Consumption Expenditures and Core PCE

|

YOY

|

NA

|

|

1.1%

|

HIGH

|

Fri. March 28

|

10:00

|

Consumer Sentiment Index (UoM)

|

Mar

|

NA

|

|

79.9

|

Moderate

|

|

|

|

The material contained in this newsletter is provided by a third party to real estate, financial services and other professionals only for their use and the use of their clients. The material provided is for informational and educational purposes only and should not be construed as investment and/or mortgage advice. Although the material is deemed to be accurate and reliable, we do not make any representations as to its accuracy or completeness and as a result, there is no guarantee it is without errors.

As your mortgage professional, I am sending you the MMG WEEKLY because I am committed to keeping you updated on the economic events that impact interest rates and how they may affect you.

If you prefer to send your removal request by mail the address is:

Jim Belote

Union Mortgage Group

582 Lynnhaven Parkway, Suite 300

Virginia Beach, VA 23452

Vantage Production, LLC is the copyright owner or licensee of the content and/or information in this email, unless otherwise indicated. Vantage Production, LLC does not grant to you a license to any content, features or materials in this email. You may not distribute, download, or save a copy of any of the content or screens except as otherwise provided in our Terms and Conditions of Membership, for any purpose.

|

|

No comments:

Post a Comment